The San Francisco Federal Reserve looks at Uncertainty and evaluates its impact on the economy.

Uncertainty is a fact of life. Long-term economic decisions are challenging because they often have long-lasting consequences and require people to make some pre-commitments. Once these decisions are made, they can be costly to reverse. For example, when people buy a house, they need to make an assumption about their future employment status and whether they will have the means to make mortgage payments. Similarly, when a business contemplates investing in a new product line, the manager must make assumptions about the strength of the economy several years ahead and how much consumers will be willing to pay for that new product. When times are uncertain, households and businesses may postpone consumption and investment decisions until they have more clarity about what lies ahead.

One indicator of uncertainty is the Chicago Board Options Exchange Volatility Index, or VIX, which measures investors’ perceptions of the 30-day-ahead volatility of the S&P 500. The VIX daily series has spiked several times since 2007. It jumped to its previous record high in November 2008, in the midst of the global financial crisis. The VIX also shot up in the fall of 2018 during a tense period of trade negotiations between the United States and China. Most recently, the COVID-19 pandemic and uncertainty about its negative impact on the world economy have ramped up the VIX to levels surpassing but comparable to those during the 2007 – 2008 global financial crisis.

In theory, heightened uncertainty can raise unemployment because a job match represents a long-term employment relationship and hiring decisions are costly to reverse. When uncertainty rises, employers may choose to wait and see before filling new positions, contributing to higher unemployment. At the same time, heightened uncertainty also reduces consumer spending because households choose to increase saving for precautionary reasons, for example, in case they lose their jobs. The decline in consumer spending reduces aggregate demand, further raising unemployment in addition to pushing inflation down.

In theory, heightened uncertainty can raise unemployment because a job match represents a long-term employment relationship and hiring decisions are costly to reverse. When uncertainty rises, employers may choose to wait and see before filling new positions, contributing to higher unemployment. At the same time, heightened uncertainty also reduces consumer spending because households choose to increase saving for precautionary reasons, for example, in case they lose their jobs. The decline in consumer spending reduces aggregate demand, further raising unemployment in addition to pushing inflation down.

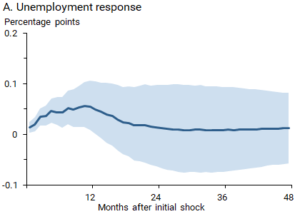

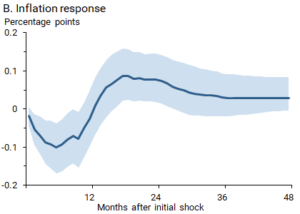

These theoretical predictions are supported by empirical evidence. Figure 2 traces out the average statistical effects of an uncertainty shock on the three macroeconomic variables in the model. Each panel shows the average as a solid line, with shading indicating a 90% certainty that the average falls within that area. Following a sudden rise in uncertainty, the unemployment rate shown in panel A rises over time, reaching a peak effect roughly one year after the impact. Similarly, panel B shows that the inflation rate falls persistently for about six months before starting to rise again. The interest rate falls quickly, reflecting monetary policy easing in response to the uncertainty shock.

The combination of a rise in the unemployment rate – that is, a decline of economic activity – and a fall in inflation suggests that uncertainty affects the economy in a way similar to a reduction in aggregate demand (Leduc and Liu 2016). Thus, through uncertainty, the COVID-19 pandemic has important demand-side effects in addition to the supply-side effects such as supply chain disruptions and labor shortages.

The combination of a rise in the unemployment rate – that is, a decline of economic activity – and a fall in inflation suggests that uncertainty affects the economy in a way similar to a reduction in aggregate demand (Leduc and Liu 2016). Thus, through uncertainty, the COVID-19 pandemic has important demand-side effects in addition to the supply-side effects such as supply chain disruptions and labor shortages.

Policy responses to supply-side effects often involve a tradeoff because supply disruptions typically push up both unemployment and inflation. If the Fed reduced interest rates to offset the rise in unemployment, it would risk further increases in inflation. Alternatively, if the Fed raised interest rates to stabilize inflation, it would risk amplifying the rise in unemployment.

In contrast, monetary policy can more easily offset the impact of a decline in aggregate demand, since cutting interest rates helps reduce unemployment and simultaneously raises inflation. Thus, demand shocks do not introduce difficult tradeoffs between the Federal Reserve’s maximum employment and price stability objectives. The decline in the interest rate following an increase in uncertainty reflects the fact that the Federal Reserve has historically attempted to offset the demand-like impact of uncertainty by cutting short-term interest rates.

Using our estimated model, we can assess the likely magnitude and duration of the macroeconomic effects of the current uncertainty spikes associated with the COVID-19 pandemic. In particular, an uncertainty shock that boosts the VIX to a level comparable to that observed in the past few weeks raises the unemployment rate by about 1 percentage point in roughly 12 months. The same uncertainty shock would reduce the inflation rate by about 2 percentage points in about six months. In turn, monetary policymakers would be expected to rapidly bring the policy rate down to the effective lower bound, as was indeed the case when the Federal Reserve cut its federal funds rate in March.

Conclusion

In addition to the tragic human toll, the COVID-19 pandemic will severely reduce economic activity as nonessential retail and other business activity is curtailed and social distancing policies and quarantines force people to stay home. The negative impact on the economy can be further amplified and prolonged by rising uncertainty. Our estimates suggest that the spikes in uncertainty triggered by the COVID-19 pandemic will contribute to a protracted increase in unemployment and a significant decline in the inflation rate in the United States. The Fed’s decision in March to cut the federal funds rate to a near-zero level can partly cushion these demand-like effects resulting from the more uncertain environment.