Category Archives: Finance

European Banks Need Further Overhaul?

If you had to pick the moment when European banking reached the point of no return, which would you choose? The July day in 2012 when Bob Diamond resigned as Barclays’s chief executive officer amid the Libor rigging scandal? Or the fall morning later that year when UBS announced it was pulling out of fixed income and firing 10,000 employees? How about Sept. 12, 2010, when Basel III’s raft of costly capital requirements started upending the economics of global finance?

All signature events, to be sure. But try May 21, 2015. That’s when 40 per cent of Deutsche Bank stockholders gave co-CEOs Anshu Jain and Jürgen Fitschen a big thumbs down. By the end of June, Jain was out and Fitschen had agreed to leave the company by May of this year.

Illustration by David Foldvari

Investors are running out of patience with European bank chieftains, and no wonder. Since the fall of Lehman Brothers in September 2008, eight of Europe’s biggest banks have announced layoffs adding up to about 100,000 employees, paid $63 billion in legal penalties, and lost $420 billion in market value. In 2015, Deutsche Bank lost a record €6.8 billion ($7.6 billion). In mid-February the industry suffered an epic selloff as subzero interest rates, China’s slowdown, the oil crash, and looming regulatory and litigation costs triggered an outbreak of fear not seen since the fall of 2008. Just last year new CEOs took over at Barclays, Credit Suisse, Deutsche Bank, and Standard Chartered.

Credit Suisse’s new CEO, Tidjane Thiam, is “right-sizing” the investment bank and pushing for a 61 percent jump in pretax income from his international wealth management unit over the next two years. At Barclays, Jes Staley wasted no time cutting 1,200 investment banking jobs and closing offices in Asia and Australia after taking charge in December. Meanwhile, John Cryan, the British executive who replaced the India-born Jain, is pursuing an unprecedented overhaul of Deutsche Bank’s entire information technology infrastructure to shore up shaky risk-management systems.

Deutsche agreed to pay $2.5 billion in penalties to U.S. and U.K. authorities for its role in the Libor rate rigging. (No current or former member of the bank’s management board was implicated.) But something deeper was at work, too. European banks aren’t going through a stormy phase that will eventually clear and permit them to claim a new golden age.The industry is undergoing a metamorphosis that will demand a thorough and radical alteration of its core operating model.

Health Care Technology Jobs Market Strong

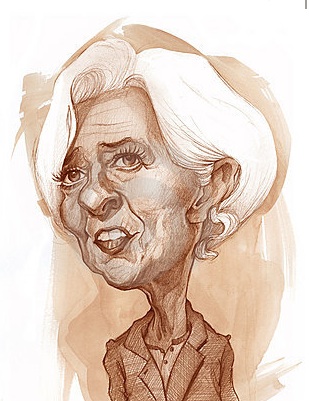

Lagarde Re-Upped

For the past five years, Christine Lagarde’s face has been splashed across the media above headlines pertaining to the International Monetary Fund (IMF). Lagarde has been one of the most visible leaders of an international economic organization in recent history, and the leadership of the IMF has noticed. As a result, Lagarde has been nominated to serve a second five-year term as the head of the International Monetary Fund.

The IMF is a made up of 188 member countries, and carries the mandate of ensuring the stability of the world’s monetary system. It does this via a system of exchange rates, loans, and international payments. These systems allow countries around the world to smoothly transact business with one another. To be sure, this is not an easy task.

Lagarde’s illustrious background includes serving as the French Finance Minister before becoming the first female director of the IMF in 2011. She was the only person nominated for the role of IMF chief this term. Observers have pointed out that Lagarde’s charisma, strong leadership, and intelligent choices, both politically and as a matter of policy, meant that there were no other obvious choices to fill the position.

Lagarde, now 60, has done a supreme job of unifying otherwise contentious factions behind her work and her vision for the IMF. Her nomination for a second term was supported by a broad cross-section of the world’s various economies, including the UK, Germany, China, and France.

According to Aleksei Mozhin, Dean of the IMF’s executive board, “The period for submitting nominations for the position of the next Managing Director of the International Monetary Fund closed on Wednesday, February 10 … One candidate, current managing director Christine Lagarde, has been nominated.” He went on to explain that the board’s goal is to complete the selection process as soon as possible to ensure the IMF’s business continues smoothly and without interruption.

Lagarde’s current term as Managing Director ends July 5, 2016. She had already announced her intention to seek a second term in January of this year, but few expected her to receive the nomination completely unopposed.

Despite the IMF’s approval, Lagarde still faces criticism in her home nation. Lagarde was recently asked to stand trial in her native country of France for alleged acts of negligence pertaining to a 2008 payment made to businessman, Bernard Tapie. Lagarde’s attorney called the decision to make her stand trial “incomprehensible” and noted that she would appeal.

Will Brazil’s Rough Patch Become a Swamp?

Otaviano Canuto writes: After decades of rapid economic growth and per capita income gains, Brazil is struggling. According to the International Monetary Fund, the country’s GDP is poised to contract by more than 7% in 2015-2016. No single factor explains this reversal of fortune. Four do.

For starters, there is the structural trend of rising primary government expenditure as a share of GDP, which reached 36% in 2014, up from 22% in 1991.

The second factor shaping Brazil’s fortunes is the commodity-price super cycle. The upswing in commodity prices that began in 2004 brought many benefits for Brazil: external surpluses, the accumulation of foreign-exchange reserves, positive wealth effects, and higher investment in natural-resource-related sectors. Add to that exchange-rate appreciation and rising minimum-wage floors – not to mention public-sector disbursements indexed to the latter – and Brazil enjoyed a virtuous domestic cycle featuring positive feedback loops between demand for services and formal employment.

The problem is that Brazil allowed high commodity prices simply to reinforce the underlying growth model, instead of preparing its economy for the inevitable bust. Profitability levels in the manufacturing industry were crushed by exchange-rate appreciation and rising domestic production costs, and levels of production practically stagnated from 2008, before starting to decline in 2014. When world metal prices began to fall in 2011, followed by food prices in 2014, Brazil’s economy lost its growth engines.

Brazil’s government did make adjustments to its growth pattern following the global financial shocks of 2008-2009. But it took a shortcut, relying on counter-cyclical fiscal and monetary policies to boost growth. This is the third key factor contributing to Brazil’s current travails.

Given structural factors, however, the main outcome of this second round of stimulus was fiscal deterioration.

Over the last year, Brazil has been struggling to unwind that attempted shortcut. The realignment of regulated prices with market prices, together with that of foreign and domestic prices (through exchange-rate depreciation), produced an inflation shock, with the consumer-price index reaching a 13-year high last year. In order to contain the shock and control inflation expectations, Brazil’s central bank was driven to increase interest rates.

The fourth factor undermining Brazil’s economic performance arose unexpectedly last year, when a multibillion-dollar corruption scandal engulfed the state-controlled oil company Petrobras, prompting a far-reaching investigation of high-level politicians and triggering a collapse of private investment.

The medium-term silver lining is that the Petrobras investigation demonstrates Brazil’s commitment to the rule of law, implying that the country’s reputation among investors will recover.

In an effort to minimize the budget deficit, the authorities have proposed new tax measures, including new rules on capital gains and the reenactment of a tax on financial transactions. Given the current dependence of taxation on consumption and the ongoing current-account adjustment, the tax on financial transactions, in particular, will be vital to buy time for mandatory public expenditures to be reviewed. Among the expenditures that will come up for review are pensions, as social security expenditure probably reached close to 8% of GDP last year. Efforts to make the labor market more flexible and reduce the cost of tax compliance will also help to improve Brazil’s investment climate.

To recapture strong and reliable growth, however, the key will be improved confidence – and that hinges largely on the government’s capacity to overcome the current political crisis. If it fails, Brazil’s current economic rough patch could well turn into a swamp.

Effective Anti-Corruption Techniques?

Bjorn Lomborg writes: Some $1 trillion was lost to corruption last year. This is money that was not available for expanding health care, broadening access to education, improving nutrition, or cleaning up the environment. According to Transparency International, 68% of the world’s countries have a serious corruption problem, and no country is completely immune.

Corruption is one facet of poor governance; indeed, it correlates with ineffective public administration, weak accountability, low transparency, and inconsistent implementation of the rule of law. So it is little wonder that the United Nations’ brand-new Sustainable Development Goals, coming into force this year, aim to fight it. Nonetheless, the SDGs represent a departure from the previous development framework, the Millennium Development Goals, which contained no explicit targets relating to corruption.

The problem is that the SDGs have so many targets – 169 in total – that they promise virtually everything to everyone. Without enough time or resources to focus on everything, countries will prioritize.

Nobel laureate economists identified 19 super-targets that would do the most good for the world for each dollar spent. These include achieving universal access to contraception, stepping up the fight against tuberculosis, and expanding preschool access in Sub-Saharan Africa. The economists recommended that the world’s donors and governments focus first on these investments.

The UN’s 12 corruption and governance-related targets weren’t among these phenomenal investments. One reason is that several of the UN’s “targets” in these areas are so broad as to be meaningless. Indeed, it is all very well to say that we want to “develop effective, accountable and transparent institutions at all levels,” and to “substantially reduce corruption and bribery in all their forms,” but where do we start?

Higher wealth and economic growth lead to better governance. A study of 80 countries where the World Bank tried to reduce corruption revealed improvement in 39%, but deterioration in 25%. More disturbing is that all of the countries the World Bank didn’t help had similar success and failure rates – suggesting that the Bank’s programs made no difference.

But the experts enlisted by the Copenhagen Consensus Center found one governance-related target that actually would do some good for each dollar spent: “By 2030, provide legal identity for all, including birth registration.”

Achieving this target requires functioning public services to provide registration facilities and maintain records. Establishing such institutional capacity would create a clear model for how other services could be provided effectively. In practice, a functioning registration service would almost certainly not exist in a vacuum, and thus would be a sign of emerging administrative competence.

But this is not just about bureaucracy; there are real benefits for citizens. They can claim legal rights, including property rights, which are vital to allow individuals to prosper and the economy to grow. Likewise, elections become less vulnerable to corruption and fraud when voters are properly registered.

If we want to place a high priority on fighting corruption, we should not settle for overly broad, well-meaning slogans. We should work on specific, proven, and effective approaches such as providing legal identity for all.

But we also have to confront the possibility that when it comes to helping the world’s poor, anti-corruption policies may not be the best place to spend our money first. This is partly because there are much more effective ways to tackle problems like tuberculosis or access to contraception, and partly because current anti-corruption policies are expensive and do little or no good.

This is not to deny that corruption hits the world’s poor hard. But there are many challenges, from lack of healthcare to starvation and pollution, that also hurt the poor but that we can address more effectively.

Focusing on what we can do well seems less impressive than promising everything to everyone – until it’s time to deliver. Those who prioritize properly will end up helping many more people.

Will Legalizing Marajuana Help?

The widespread legalization of marijuana as a painkiller could help to bring America’s epidemic of opioid misuse under control. That’s the opinion of Massachusetts Senator Elizabeth Warren anyway, having spoken this weekend of the importance of national health bodies seriously and comprehensively considering regulatory change.

She spoke of the terrifying extend of prescription painkiller addiction in her letter to Thomas Frieden, head of the US Centers for Disease Control and Prevention. She made clear her belief that to explore the possibilities with legalized marijuana could make an enomous difference to a problem that’s already entirely out of control.

“Our country is faced with an opioid epidemic that only continues to grow at an alarming pace,” she wrote on Monday.

“Opioid abuse is a national concern and warrants swift an immediate action.”

“I hope that the CDC continues to explore every opportunity and tool available to work with states and other federal agencies on ways to tackle the opioid epidemic and collect information about alternative pain relief options,” she wrote.

“Your agency has produced an enormous amount of scientific and epidemiological data that has helped inform stakeholders on the breadth of this crisis — however there is still much we do not know.”

She insisted that the time had come to intelligently and realistically study the “effectiveness of medical marijuana as an alternative to opioids for pain treatment in states where it is legal,” while at the same time evaluating “the impact of the legalization of medical and recreational marijuana on opioid overdose deaths.”

Reports from the CDC suggest that opioid overdose deaths are skyrocketing across the United States each and every year – increasing more than 200% since the year 2000. Advocates argue that not only could marihuana be made available much more widely and for a lower price, but that it is considerably less addictive and almost impossible to overdose on.

Can Ukraine Survive without the IMF?

“Ukraine risks a return to the pattern of failed economic policies that has plagued its recent history.”

Lagarde’s message struck at the heart of concerns of Ukrainians who joined three months of enthusiastic but ultimately bloody protests that brought down the ex-Soviet republic’s Russian-backed leadership in February 2014.

Polls show public frustration with Poroshenko and Prime Minister Arseniy Yatsenyuk mounting and hopes ebbing away that Ukraine was finally ridding itself of mind-numbing bureaucracy and bribe-taking.

That angst was encapsulated by this month’s resignation of reform-minded Aivaras Abromavicius as economy minister in protest at alleged influence-peddling by one of the most senior members of the president’s inner circle.

The IMF chief had said bluntly that it was “hard to see how the ($40-billion, 35-billion-euro) IMF-supported programme can continue” without Ukraine making good on its promise to take radical streamlining steps ignored in the past.

Both Yatsenyuk and Poroshenko know they cannot survive without foreign assistance and that early legislative polls could return to power Russian-backed deputies who just might be enticed into warming Kiev’s frozen relations with Moscow.

Ukraine’s central bank chief warned that the mounting uncertainty was putting renewed pressure on the hryvnia just as it was starting to find its footing from a 68-percent slide against the dollar since the start of 2014.

“Without IMF support, we should expect devaluation and social instability,” said Anatoliy Oktysyuk of Kiev’s International Centre for Policy Studies.

“The alternatives (to IMF support) are not even currently being considered because they are all apocalyptic,” Oktysyuk said.

Lawmakers have already shown their resolve by blocking a constitutional change pushed by Poroshenko that the West hoped would end Ukraine’s 21-month separatist conflict by giving limited special status to pro-Russian rebel-run parts of the east.

Analysts believe that deputies’ instinctive desire to keep their jobs and avoid snap elections will keep Yatsenyuk in place and lead only to a minor government shakeup aimed primarily at preserving the current coalition intact.

“If the government fails in Kiev, it will have a direct effect on political and economic support from the West. Ukraine’s many sceptics will gain the upper hand, and its few friends will face a steep uphill struggle,” said Joerg Forbrig of the US-based German Marshall Fund policy research institute.

“Reduced assistance — whether political, financial, administrative or military — will eventually forfeit the modest gains Ukraine has made and expose the country’s many vulnerabilities,” Forbrig said.

Impact Investing by All Sectors?

Jjuerg Zeltner writes: Philanthropy’s Storming of the Bastille began in November, when a group of nearly 30 billionaires, including Amazon’s Jeff Bezos, Virgin’s Richard Branson, and Alibaba’s Jack Ma, announced the formation of the Breakthrough Energy Coalition. The BEC promised a “new model” that would leverage public-private partnerships to mobilize investment “in truly transformative energy solutions for the future.”

The announcement was closely followed by Mark Zuckerberg and Priscilla Chan’s commitment to give 99% of their Facebook shares (currently valued at some $45 billion) to improving the lives of newborns across the world. They, too, stressed the importance of “partnering with governments, non-profits, and companies.”

The game-changing development is the recognition of a funding gap – a “collective failure” of government, traditional philanthropy, and commercial investors, in the words of the BEC – that creates “a nearly impassable valley of death between promising concept and viable product.”

That is why the Chan Zuckerberg Initiative was designed for maximum flexibility, allowing funds to be channeled into non-profits, directed into private investments, or used to help influence policy debates. Similarly, the BEC has pledged to boost the work of others by taking “a flexible approach to early stage, providing seed, angel and Series A investments, with the expectation that once these investments are de-risked, traditional commercial capital will invest in the later stages.”

Of course, not even billionaires can solve the world’s problems on their own. Other stakeholders will need to play a part in the revolution as well. Traditional philanthropies should revisit their mandates. And governments must do more to facilitate a greater flow of private funds into more sustainable infrastructure assets. Policymakers could look at tax incentives, including credits in key areas.

There is an opportunity for the finance industry to participate, too, through so-called impact investing, which aims to achieve both social progress and financial returns high enough to attract mainstream private investors.

This, of course, is more easily said than done. As Bill Gates, who has given away more money than anyone in the history of the world, put it: “So many things have a social return, but not a financial return. You really have to be careful thinking you can have your cake and eat it.”

That is especially true for those who design financial instruments for impact investing. Among the most innovative are development impact bonds, in which investors provide financing for development projects, in exchange for returns provided by donors, NGOs, or government agencies if, and only if, the agreed-upon outcomes are achieved.

For example, one such bond is funding an effort to enroll and keep girls in school in Rajasthan, India. Depending on the program’s attendance rates and success at imparting numeracy and language skills, the Children’s Investment Fund Foundation will pay a return to bondholders. Programs like this, it is hoped, will provide a model that can be replicated and scaled up elsewhere.

Another promising opportunity are investments in the riskiest stage of the development process for new drugs: the phase between basic research and human clinical trials, which has traditionally struggled to attract funding. Indeed, for every $1 million dollars spent on this part of the process, some $8 million is spent on basic research and another $20 million on clinical trials.

Quarterly earnings cycles, real-time pricing, and constant scrutiny by shareholders have pushed pharmaceutical companies toward projects with clear, immediate payoffs – at the expense of more speculative, but potentially transformational research. With interest rates at record lows in much of the developed world, major players in the financial system have an opportunity – and, I would add, a responsibility – to help bridge this gap. In addition to providing a robust social impact, a patient investment strategy in this area would also offer high long-term financial returns.

There is a strong desire on the part of many in the finance industry to make investments that improve the world. The revolution in philanthropy will be truly successful only when we realize that we do not have to be billionaires to make a difference.

Can China Bounce Back?

Keyu Jin writes: Pessimism about China has become pervasive in recent months, with fear of a “China meltdown” sending shock waves through stock markets worldwide since the beginning of the year. And practically everyone, it seems, is going short on the country.

There is certainly plenty of reason for concern. GDP growth has slowed sharply; corporate-debt ratios are unprecedentedly high; the currency is sliding; equity markets are exceptionally volatile; and capital is flowing out of the country at an alarming pace. The question is why this is happening, and whether China’s authorities can fix it, before it is too late.

The popular – and official – view is that China is undergoing a transition to a “new normal” of slower GDP growth, underpinned by domestic consumption, rather than exports. And, as usual, a handful of economic studies have been found to justify the concept. But this interpretation, while convenient, can provide only false comfort.

China’s problem is not that it is “in transition.” It is that the state sector is choking the private sector. Cheap land, cheap capital, and preferential treatment for state-owned enterprises weakens the competitiveness of private firms, which face high borrowing costs and often must rely on family and friends for financing. As a result, many private firms have turned away from their core business to speculate in the equities and property markets.

Chinese households are also squeezed. In just 15 years, household income has fallen from 70% of GDP to 60%.

China has proved its capacity to implement radical reforms that eliminate major distortions, thereby boosting growth and absorbing excess debt.

The Chinese government launched a raft of radical reforms, including large-scale privatization of industry and elimination of price controls and protectionist policies and regulations.

This time around, however, the task facing China’s government is complicated by political and social constraints. The economic reforms China needs now presuppose political reform; but those reforms are hampered by fears of the social repercussions.

The good news is that China has a promising track record on this front.

A similar ideological shift is needed today, only this time the focus must be on institutional development. S

With a concerted effort to create a level playing field that gives more people a bigger piece of the economic pie, not to mention more transparent governance and a stronger social safety net, China’s government could reinforce its legitimacy and credibility.

China’s experience in the 1990s suggests that the country can bounce back from its current struggles.

If economic conditions worsen, as seems plausible, action will become unavoidable. Good times may breed crises in the West; in China, it is crises that bring better times.