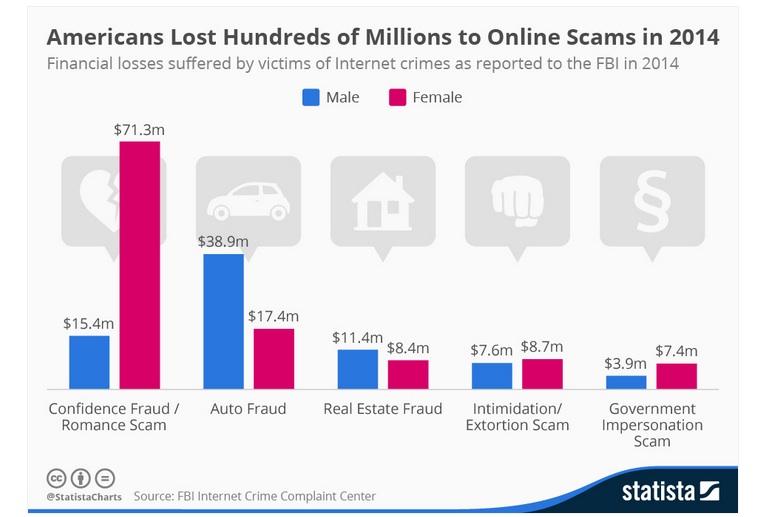

The IC3 received 269,422 complaints consisting of a wide array of scams affecting victims of all demographic groups.

The most frequently reported crimes are broken down in the chart below, which also illustrates how different scams are targeted at different demographics. While confidence / romance scams, in which the criminal establishes an online relationship with its victim and later asks for money, are mostly targeted at middle-aged women, men are more likely to fall for too-good-to-be-true car listings and become victims of auto fraud.

For more information on the different kinds of online scams visit the IC3’s website or check out its latest annual report on Internet crime.

This graphic charts the financial losses suffered by victims of Internet crimes in the United States in 2014.

Amadou Sy writes: As they prepare for the fast-approaching Third International Conference on Financing for Development in Addis Ababa (July 13-16, 2015), policymakers, private sector actors, and other global leaders should examine the types of external financial flows (defined as the sum of gross private capital flows, official development assistance (ODA), and remittances) that different groupings of countries receive in order to best support the implementation of the post-2015 development agenda. Understanding how different sources of development finance flow to different parts of Africa can help identify priority areas of intervention.

External financial flows to sub-Saharan Africa have increased significantly over the past 20 years or so. In fact, the volume of external flows reached about $120 billion in 2012—from $20 billion in 1990.

But to what extent have these changes in the scale and composition of external flows to sub-Saharan Africa equally benefited countries in the region? Did the rising tide lift all boats? Is aid really dying? Are all countries attracting private capital flows and benefiting from remittances to the same degree? Finally, how does external finance compares with domestic finance?

We find that the type of external financial flow to non-resource-rich high-growth (NRRHG) and fragile states/low-income countries differs significantly from that of both middle-income and oil-exporting countries. Our main finding is that changes in both the scale and composition of external capital flows have not benefited all sub-Saharan African countries equally. We also find that the claim of the demise of aid is premature, the growth of private capital flows has benefited only a few countries, remittances have become significantly more important for some countries, and the rise of external flows means that sub-Saharan African countries will have to manage the volatility associated with such flows. In particular, we find that:

Fragile countries and LICs, not surprisingly, are regional laggards in terms of access to both external and domestic finance.

Even resource-rich countries, which are able to attract large volumes of private capital flows, fare relatively poorly when external financing flows are scaled to the size of their economies. In addition, these countries, although they raise more domestic government revenues than other countries, do so mostly because they benefit from fiscal revenues linked to volatile commodity prices.

Francophone countries both in the WAEMU and the CEMAC are not able to attract the same level of private capital flows as other sub-Saharan African countries. Remittances are high for middle-income countries. When external financing is contrasted with domestic financing, it seems that sub-Saharan African countries do not appear to have a natural hedge to the risks of reversal of external financial flows.

Andrew Sheng and Geng Wiao write: The People’s Bank of China has cut interest rates for the third time in six months, in order to lighten the debt burdens of companies and local governments. But the PBOC’s monetary easing – accompanied by complementary fiscal and administrative adjustments – has done little to increase demand for new loans. Instead, it has triggered a sharp rise in China’s stock markets. The question now is whether that could turn out to be a very good thing.

There is little doubt that China’s economy is shifting gears very quickly. Official statistics show a slowdown in real growth in the old manufacturing and construction-based economy, reflected in declining corporate profits, rising defaults, and an increase in non-performing loans in poorer-performing cities and regions.

With harder budget constraints imposed by the central government, local officials and state-owned enterprises (SOEs) have curbed their spending which could lead to localized balance-sheet recessions.

Increased innovation and the rise of the services sector have helped China move beyond its role as the world’s factory to develop its own version of the Internet of Things, driven by platform companies like Alibaba and Tencent.

Some 14.3 million new stock-market trading accounts were opened in China last year. The revival of China’s stock market in a low-interest-rate environment represents an important shift in asset allocation away from real estate and deposits. Roughly 50% of Chinese savings – amounting to as much as half of GDP – lie in real estate alone, with 20% in deposits, 11% in stocks, and 12% in bonds.

Rising stock-market capitalization also helps to reduce the real economy’s exposure to bank financing. The US is much more “financialized” than China, with stocks and bonds amounting to 133% and 205% of GDP, respectively, at the end of 2013. Those ratios were only 35% and 43%, respectively, in China.

But the rapid run-up in equity prices also carries considerable risks – namely, the possibility that the financial sector will misuse the newfound liquidity to finance more speculative investment in asset bubbles, while supporting old industries with excess capacity.

Even if Chinese retail investors begin to channel their money toward innovative ventures, identifying the companies and industries most likely to succeed will be difficult.

As China’s animal spirits are channeled, they will increasingly test the authorities’ resolve to resist price intervention, instead allowing market forces to propel the business cycle.

Indeed, at the end of last year, China still had CN¥22.7 trillion of statutory reserves, amounting to 36% of GDP, that had long been used to “sterilize” its large foreign-exchange holdings.

Lee Jong-Wha writes: By the end of this year, the International Monetary Fund will decide whether the Chinese renminbi will join the euro, the Japanese yen, the British pound, and the US dollar in the basket of currencies that determines the value of its international reserve asset, the Special Drawing Right (SDR).

The IMF created the SDR in 1969 to supplement existing reserve currencies, thereby providing the global financial system with additional liquidity.

To qualify for inclusion, the Chinese government has eased its capital controls and liberalized its financial markets considerably. Yet the US, in particular, reluctant to welcome China into the fold.

This is all the more problematic given that the 2008 financial crisis laid bare the international reserve system’s inadequacy when it comes to ensuring sufficient liquidity for emerging economies.

This continued vulnerability reflects a collective failure to reform the global monetary system. China has championed a transition to a multi-currency reserve system, in which the SDR and an internationalized renminbi would be used more widely, including in countries’ currency reserves. But its attempt in 2010 to add its currency to the SDR basket failed, because the renminbi was not “freely usable.”

Since then, China has implemented a series of reforms to increase the renminbi’s usage in foreign trade and direct investment, as well as in cross-border financial investment. Fourteen renminbi-clearing banks have been established worldwide

Chinese policymakers have signaled further financial liberalization by removing the domestic cap on banks’ deposit rates, thereby giving overseas institutional investors easier access to capital markets. The PBOC is also likely to widen the currency’s trading band and move toward a more flexible exchange-rate regime.

As a result of these efforts, the renminbi has emerged as the second most used currency in trade finance.

Of course, China stands to gain much from the renminbi’s emergence as an alternative international reserve currency.

But China must confront significant risks. Capital-account liberalization and renminbi internationalization invite potentially volatile cross-border capital flows, which could, for example, trigger rapid currency appreciation.

Even if China manages to mitigate such risks, unseating the US dollar as the dominant global currency will be no easy feat. Inertia favors currencies that are already in use internationally, and China lacks deep and liquid financial markets, an important precondition that any international reserve currency must meet.

If, however, China succeeds in developing a more convertible capital account and bolstering its financial system’s efficiency, the renminbi is likely to emerge as a new international reserve currency, complementing the US dollar and the euro.

For now, China is focused on winning the renminbi’s inclusion, even with a small share, in the SDR currency basket. The IMF’s major shareholders should seriously consider it. The renminbi’s continued internationalization, not to mention further progress on critical financial reforms, would contribute to the creation of a more stable and efficient global reserve system.

Samura Kamara writes: China’s decision to establish the Asian Infrastructure Investment Bank has sparked a lively debate among governments, global finance experts, and development specialists.

The mandates of individual development banks vary. The AIIB, for instance, will focus solely on infrastructure. The African Development Bank (AfDB), the presidency of which I am currently seeking, has a far more expansive mandate. But all of these institutions share an overarching goal: to lift people out of poverty and foster sustainable development.

Leaders of these organizations must make complicated choices in allocating their finite resources. For example, they must balance the battle against poverty and hunger against efforts to improve gender equality, increase access to education, or tackle corruption.

Fifteen years ago, the world adopted the Millennium Development Goals to achieve specific targets for improving human welfare in the new century. Today, despite the MDGs’ notable successes, too many of the targets remain unachieved. As the world prepares to agree upon new Sustainable Development Goals to succeed the MDGs, we must put in place the policies needed to ensure that the targets can be met.

A prerequisite for the success of any development bank or other multilateral institution is adherence to the highest standards of transparency and accountability.

Proper regulation and scrutiny is crucial to an international organization’s success, and robust environmental, labor, and procurement standards are essential to the mission of all development lenders. These institutions’ leaders must always remember for whom they are ultimately working; local communities must be empowered to play a role in shaping the development agenda, and more must be done to engage with them directly, through a fully devolved structure.

Mechanisms of accountability are not just auditing devices. Such lenders should not operate in a vacuum. Many governments possess years of accumulated institutional knowledge. Lending institutions that not only provide money, but also exchange ideas, can significantly improve the outcome of their work.

Indeed, by sharing knowledge, methods, and research with their peers and partners, organizations like the AfDB are better-placed to ensure that the highest standards and best practices are widely adopted.

The AfDB has already incorporated many of these practices into its operating framework, providing it with a foundation for continued growth and service. Those putting in place the policies, personnel, and practices of the AIIB would be wise to adhere to this model.

Soutik Biswas writes: Mr Modi ran a presidential-style campaign, promising achhe din, or better times, if elected. It is a promise which his supporters continue to cling to, and his detractors sneer at, saying it was a deceit to capture political power.

A poll by Mint newspaper found the prime minister has an approval rating of 74%, although down eight percentage points since last August. Another poll by the Times of India found 47% of the respondents saying that Mr Modi’s performance in government had been “somewhat good”, and an ambivalent quarter saying that it had been “neither good, nor bad”.

In truth, Mr Modi faces little competition: the Congress party, under Sonia and Rahul Gandhi has still not recovered from last year’s debacle, despite the latter’s spirited recent efforts to pick up the gauntlet. India’s Grand Old Party remains largely bereft of new ideas to fire the imagination of India’s restless young, who form the bulk of voters.

Inflation has been tamed, and the fiscal deficit contained. For both, Mr Modi should thank cheap commodity – mainly oil – prices. Electricity generation has surged to a record high.

His government so far has been free of scams, and he is making his ministers and bureaucrats work hard. Plans to auction mineral rights – starting with this year’s coal auction – should check corruption and foster transparency. He has energised India’s foreign policy, openly courting countries like Japan, Australia, Israel and the US. He is mining the diaspora. Taking the lead in evacuating stranded people in conflict-zones like Yemen and rushing relief to earthquake-ravaged Nepal has earned his government rightful praise. “Two foreign policy priorities have emerged: South Asia and the management of a larger periphery with a focus on China,” says Harsh V Pant of King’s College, London.

There are reports of industrialists, bureaucrats and politicians saying that corruption at the top has “declined dramatically”.

But all of this is still not translating into a resurgent economy: companies are not performing well, industrial output is flat, bank credit is languishing, the property market is gloomy.

The goods and services tax, India’s single biggest tax reform after Independence, appears to be embroiled in familiar political differences, and many believe that a watered down version is now being pushed through in what is seen as a shoddy compromise..

There is talk about reducing bloated government, but no radical reforms seem to be on the table. Some of Mr Modi’s ambitious projects so far look like retreads of older ones. Failure to fix the basics could easily hobble each programme.

Mr Modi wants to set up 100 smart cities, but most of India’s main cities have turned into urban dystopias. Nobody quite knows what Digital India means in a country where the elementary mobile telephone network is broken.

Mr Modi raised massive hopes of transforming India; the tyranny of high expectations can bite badly.

Some 13 million Indians are seeking jobs every year, and if Mr Modi cannot get them work, he won’t have their votes. This is no longer an India which is endlessly willing to wait patiently. Mr Modi must know that – and that he needs to do more.

Angela Stanzel writes: Since 2013, China has been hyping its New Silk Road project. It launched a massive public relations campaign – which even held out the prospect of “Silk Road Tourism” – to turn the idea of a global transportation network into an incentive to cooperate with China and an expression of an Asian “community of destiny”. But China will face huge challenges in making the New Silk Road a reality. One of the places where China had begun re-construction of ancient Silk Road links early on is Pakistan. But after decades, progress has been limited. Despite China’s commitment to the Silk Road project, it’s not clear that it is going anywhere.

The “Belt and Road” initiative” includes two elements, a Silk Road Economic Belt and the 21st Century Maritime Silk Road; the aim is to create a northern road corridor and a southern maritime corridor to connect China with Europe. Beginning with Jiang Zemin in 1996, the Silk Road narrative has been long used by Chinese leaders to increase China’s – mainly economic – cooperation with other countries in Central Asia, South Asia and the Middle East, Africa – and in Europe. Since 2013, the new Chinese leadership under Xi Jinping has developed this narrative that integrates existing projects in two mega “Belt and Road” initiatives.

The Silk Road initiative has also given a new impetus to China’s infrastructure development in Pakistan. China’s construction of the Karakoram Highway/Road from China to Pakistan dates back to the beginning of the 1970s – long before the “Silk Road” hype of the last few months. China has financed and developed the Gwadar port on the Arabian Sea since the 1990s. Since 2013, China and Pakistan have been planning a China-Pakistan Economic Corridor, which connects Gwadar with China’s western Xinjiang region. According to Chinese president Xi Jinping, the Economic Corridor is “a major project of the ‘Belt and Road’ initiative” How Does the Silk Road Wind

Roping off the Middle East and letting them solve their own problems sounds like a good idea, but simply won’t work. President Obama is facing the problem head on. Here is an interview by Jeffrey Goldberg in which the President describes his plans and hopes.

Tensions between the U.S. and the Gulf states, I came to see, have not entirely dissipated. Obama was adamant on Tuesday that America’s Arab allies must do more to defend their own interests, but he has also spent much of the past month trying to reassure Saudi Arabia, the linchpin state of the Arab Gulf and one of America’s closest Arab allies, that the U.S. will protect it from Iran. One thing he does not want Saudi Arabia to do is to build a nuclear infrastructure to match the infrastructure Iran will be allowed to keep in place as part of its agreement with the great powers. “Their covert—presumably—pursuit of a nuclear program would greatly strain the relationship they’ve got with the United States,” Obama said of the Saudis.

In the wake of what seemed to have been a near meltdown in the relationship between the United States and Israel, Obama talked about what he called his love for the Jewish state; his frustrations with it when it fails to live up to both Jewish and universal values; and his hope that, one day soon, its leaders, including and especially its prime minister, will come to understand Israel’s stark choices as he understands Israel’s stark choices. And, just as he did with Saudi Arabia, Obama issued a warning to Israel: If it proves unwilling to live up to its values—in this case, he made specific mention of Netanyahu’s seemingly flawed understanding of the role Israel’s Arab citizens play in its democratic order—the consequences could be profound. Obama and the Middle East

Yves Smith writes; SEC Commissioner Kara Stein has waged an uphill battle to have the agency stop giving financial firm miscreants waivers from sanctions that would otherwise take effect when they enter into settlements for bad conduct. Stein took issue with the SEC’s prior stance, that these “get out of jail” cards were issued freely to big firms by virtue of simply asking for them. The tacit assumption seemed to be that these firms were big reputable players and hence imposing the normal legally-mandated sanctions was overkill. In fact, as we know too well, the behemoth banks do disproportionate harm by their bad actions, and recent history has shown that they’ve misbehaved across a large swathe of businesses.

Despite the fact that a single SEC commissioner has limited power, Stein has managed to stymie the granting of some of these waivers by teaming up with like-minded SEC Commissioner Luis Aguilar on cases where Chairman Mary Jo White has had to recuse herself. Stein and Aguilar’s opposition to granting waivers on a recent Bank of America settlement led to further negotiations that imposed additional requirements upon the Charlotte bank. Stein and Aguilar has also been pushing for tougher punishments, including lifetime bans from SEC regulated entities for bank executives who break securities laws.

Below is Stein’s dissent on the granting of waivers to the five banks that admitted to a criminal conspiracy to rig the spot foreign exchange market in dollars and Euros. As Stein points out, the issue isn’t just the severity of this particular incident; it’s that theses firms are recidivist bad actors yet have been granted waivers on the barmy presumption that they are for the most part, corporate citizens in good standing.

Ian Talley writes: The Obama administration, facing a push by U.S. lawmakers to insert language that targets currency manipulation in a major Pacific trade deal, is pitching a less-aggressive approach that would bolster international oversight and transparency of currency policies.

The Treasury Department says the “historic new approach” it envisions would bring exchange-rate provisions into trade negotiations for the first time and strengthen U.S. efforts to persuade countries not to use their currencies to gain unfair competitive advantages.

The administration hopes its strategy would help fend off efforts—largely by members of the president’s own party—to include provisions for binding sanctions against currency manipulators. The White House says those measures would sink the Trans-Pacific Partnership trade deal, a pillar of President Barack Obama’s plan to boost the U.S. economy and fortify economic and strategic ties in Asia.

The Senate late Friday passed legislation on what is known as fast-track authority, propelling the bill toward what is expected to be an even-more difficult path in the House next month. The Senate rejected a currency-manipulation amendment in the measure, also known as trade promotion authority, which would allow the Obama administration to complete the trade pact with Japan and 10 other nations and bring it to Congress for up-or-down votes as soon as this fall.

The Treasury Department’s proposal—pitched to TPP member countries in recent weeks—is preliminary and faces major hurdles. One option under consideration is to require better data on the key metrics for gauging currency management such as details on foreign-currency reserves and interventions. Many countries don’t provide that data to international institutions such as the International Monetary Fund, often leaving outside economists guessing about the extent of exchange-rate interventions.