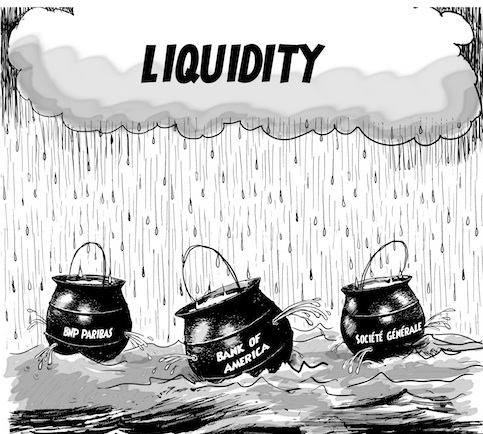

Economists at the New York Federal Reserve write: Large global U.S. banks—that is, those that have offices in foreign countries and are able to move liquidity from affiliates across borders have an advantage over large domestic U.S. banks, which have to rely on financing raised in capital markets and from depositors to extend credit and issue loans.. The internal liquidity management by global banks has, on average, mitigated the effects of aggregate liquidity shocks on domestic lending by these banks.

If a bank has stable deposit funding or maintains more liquid assets on its balance sheet, its lending might be less affected by aggregate liquidity shocks.

There also might be different responses to liquidity risk by U.S. banks that are domestically oriented compared with banks that are global. Because these two types of banks have very different business models, the channels and magnitude of transmission of liquidity risks into bank lending may differ significantly. Small domestic banks have relatively strong lending responses to liquidity risks. By contrast, banks with foreign affiliates, particularly large banks, move funds across their organizations to offset such risks, and potentially insulate lending in their home markets. However, these same banks may decrease lending abroad as they move liquidity into their home country.

For both types of banks, changes in aggregate private liquidity are likely to influence lending differently in crisis than in normal periods, in part because of the availability of and willingness to use official sector liquidity facilities in periods of aggregate liquidity stress. When banks have access to central bank liquidity facilities priced at terms below private market rates, this might relax the constraints imposed by the composition of banks’ balance sheets on their access to external funding, leading to a different relationship between those balance sheet characteristics and the banks’ lending, Is Liquidity a Measure of Stability