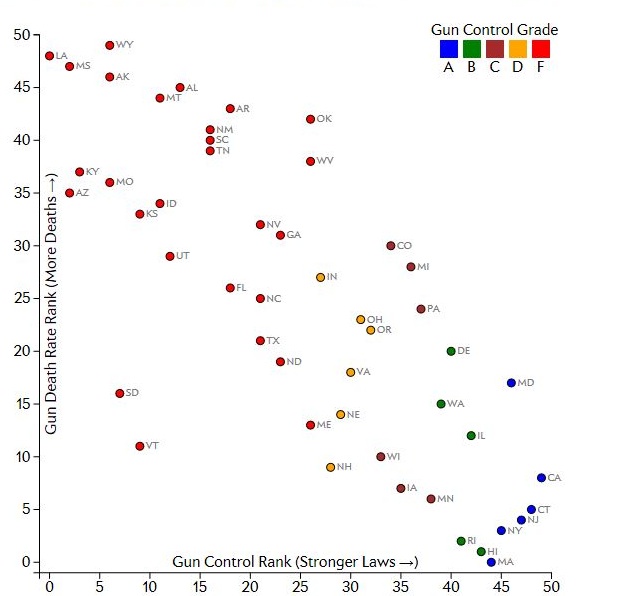

Gun deaths go down when gun control laws are stricter.

Gun deaths go down when gun control laws are stricter.

Can VW survive emissions manipulation scandal?

Volkswagen AG’s designated Chairman Hans Dieter Poetsch warned managers that the diesel-emissions scandal could pose “an existence-threatening crisis for the company.”

The German carmaker faces a Wednesday deadline to present a plan to fix some 2.8 million vehicles in its home market.

Volkswagen and German industry have been rocked by charges, first made by U.S. regulators on Sept. 18, that the carmaker had used software to hoodwink regulators about the true emissions of its diesel cars for years. As owners of 11 million affected cars across the globe, regulators and investors await answers, the crisis has wiped out almost 30 billion euros ($34 billion) of the company’s value.

After mostly remaining silent on the cheating scandal, ChancellorAngela Merkel on Sunday called the disclosure by Germany’s largest carmaker “a dramatic event” and said Volkswagen must clarify the affair swiftly. She ruled out a longer-term impact on the country’s industry.

An internal investigation has already yielded several engineers who admitted to installing the fraudulent software in 2008 for EA 189 diesel-motor models. The result was a so-called defeat device that disengaged emissions controls when an auto wasn’t being tested, breaching emissions rules and prompting a raft of government investigations and lawsuits since the U.S. Environmental Protection Agency cited the violations last month.

Volkswagen has also found more executives are involved in the scandal than previously acknowledged.

The manipulated software may have been put into parts supplied by Hanover, Germany-based Continental AG for 1.6-liter engines. Upgrading models with Continental parts would entail replacement parts, not just a software upgrade, Bild said.

Another engine-parts supplier, Robert Bosch GmbH, warned VW in 2007 that its planned use of the software was illegal.

In contrast with Merkel, European Parliament President Martin Schulz, a German Social Democrat, said the scandal is a “grave blow for the German economy as a whole.”

First, we have to remember that women often get the top job when a company is in trouble. Note HP and GM in the US>

Megam McArdle writes: Justin Fox notes that HP was in a hard place, Jeffrey Sonnenfeld argues Fiorina seems indisposed to admit to and learn from her failures. Fiorina wasn’t the best CEO in history, she certainly wasn’t the worst, either.

Critiques of Fiorina’s tenure seem excessively focused on the outcome. People are far too prone to confuse outcomes with good decision-making. Too many of Fiorina’s critics pointed out that the company lost shareholder value, then settled back with a satisfied QED.

The merger Fiorina spearheaded with Compaq was costly and did not noticeably improve the company’s competitive position. The company stock price certainly did fall a lot from the time she started there to the time she finished (something that unsurprisingly happens to a lot of CEOs before they’re forced out). A lot of employees were laid off in the process of making a larger, less profitable company.

This does not mean that Fiorina did a bad job. Fox makes this point: The strategy she started paid off much better after she left, but she gets no credit for it. I’d like to make a different, if related point: Sometimes, CEOs don’t really have any good options.

At the time Fiorina took over, HP made a fine server and a nice workstation and a very good printer. But it had become clear that the hardware business wasn’t such a great place to be. In fact, that had been true for a while, but until the late 1990s, there was some hope that things would shake down to a few players, prices would stabilize, and things would get better, as had happened in the automobile market.

Did Fiorina manage to fix this problem? Not really. But it’s far from clear to me that anyone else could have fixed it, given that she presided over a difficult business model during the Great Tech Meltdown and the recession that followed. Her idea to merge with Compaq, in order to give the company enough scale to take on IBM in the corporate market, didn’t work out as she’d hoped, but while that’s obvious in hindsight, it was undoubtedly a mite harder to see at the time.

Failure doesn’t always mean that you made the wrong decision. It might just have meant that there were no good options, or that you got unlucky.

Fiorina could be the best CEO in the world, or the worst, and that wouldn’t give us much insight into how she’d do as president.

We’re in the midst of a great outsider boom, from Bernie Sanders to Donald Trump, to populist parties in Europe and the election of a far-left Labour backbencher as leader of the party in the U.K. Much of the appeal seems to be that we need someone to shake things up who’s not beholden to the same tired, focus-grouped, compromised, corrupt political culture. On the left, this appetite seeks out radical firebrands who promise they won’t sell out to the neoliberal consensus; on the right, it looks to business leaders (or maybe surgeons), who have proved they are competent in a competitive domain utterly unlike the political system.

This is another way of committing the fundamental attribution error. Politicians are the way they are because they operate under serious constraints.

The closest job is either head of another government (most of whom are not legally eligible to run for U.S. president) or governor (few of whom have any foreign policy experience).

The problem, in other words, is not the people or the “culture” they live in; it is the system. And at least politicians know how to get results out of that system, however puny those results may seem next to our grand dreams of wholesale change. They do this largely by means of the very things we hate about them: staying within fairly narrowly plausible lines, compromising, trading favors, catering to single-issue interest groups, focus-grouping and poll-testing everything to death. An outsider may not do any of those things. But if not, they won’t do much else, either.

Yves Smith writes: The Department of Justice may face an early test of its long-overdue policy change, that the government will seek to prosecute individuals, including executives, along with those of corporations. As Sally Yates, Deputy Attorney and author of the memo setting forth the new policy, put it, “We mean it when we say, ‘You have got to cough up the individuals.’”

Private plaintiffs have filed two suits alleging bid-rigging by the 22 primary dealers, adding pressure to an ongoing Department of Justice investigation.

The same analytical technique that uncovered cheating in currency markets and the Libor rates benchmark — resulting in about $20 billion of fines — suggests the dealers who control the U.S. Treasury market rigged bond auctions for years, according to a lawsuit….

The plaintiffs built their case against the 22 primary dealers who serve as the backbone of Treasury trading — including Goldman Sachs Group Inc., JPMorgan Chase & Co. and Morgan Stanley — using data from Rosa Abrantes-Metz, an adjunct associate professor at New York University who has provided expert testimony in rigging cases.

Bear in mind that investigations and litigation is underway, and no charges have yet been proven. However, in the last major Treasury bid-rigging scandal, in 1991, the Fed didn’t bother to wait for the Department of Justice to act. SEC Says- Cough Up Individual Wrongdoers

Howard Davies writes: In 1993, the economists Alberto Alesina and Larry Summers published a seminal paper that argued that central bank independence keeps inflation in check, with no adverse consequences for economic performance. Since then, countries around the world have made their central banks independent. None has reversed course, and any hint that governments might reassert political control over interest rates, as happened recently in India, are met with alarm in financial markets and outrage among economists.

In truth, however, there are many degrees of independence, and not all nominally independent central banks operate in the same way. Some monetary authorities, like the European Central Bank, set their own target. Others, like the Bank of England (BoE), have full instrument independence – control over short-term interest rates – but must meet an inflation target set by the government.

There are differences, too, in how central banks are organized to deliver their objectives. In New Zealand, the bank’s governor is the sole decision-maker. At the US Federal Reserve, decisions are made by the Federal Open Market Committee (FOMC), whose members – seven governors and five presidents of the Fed’s regional reserve banks – enjoy varying degrees of independence. The Independence of Central Banks

Larry Elliott writes: The fresh dose of deflationary measures in Greece’s new €86bn (£62bn) bailout programme, agreed in July after Tsipras folded under pressure from creditors, will deepen a depression similar in its severity to those that afflicted Germany and the United States in the 1930s.

The Greek economy has contracted by 29% since 2009 and is still shrinking after months of financial turmoil. Yet Greece remains part of a single currency that has emerged bloodied but intact. All the main parties contending the election were committed to continuing with the bailout that Tsipras negotiated in the summer.

Even so, the election will have consequences. Syriza has done well enough to form a workable coalition, thereby avoiding the need for another election and removing one of the hurdles before Greece has the first review of its bailout some time before the end of the year.

Dallas Fed reports:

|

by Jesus Canas and Emily Gutierrez Mexico is a country of contrasts, its geography varying from deserts to jungles, mountains to beaches. Such differences extend to the economic characteristics of Mexico’s four regions: the manufacturing north, the agrarian north-central, the service-based central and the energy-producing south.

Such economic specialization has contributed to significantly different levels of development – evident in persistent and often worsening disparities in standards of living. Mexico’s affluent north is characterized by a large manufacturing base, which sharply diverges from the poverty-stricken south, a hub of energy activity. The central region benefits from the sprawling reach of Mexico City, one of the world’s largest metropolitan areas and the heart of the Mexican economy, while the agriculturally driven northcentral zone makes a much smaller economic contribution. Outlook Mexico |

Asli Demirgüç-Kunt and Enrica Detragiache, World Bank, Development Research Group, and International Monetary Fund, Research Department write:

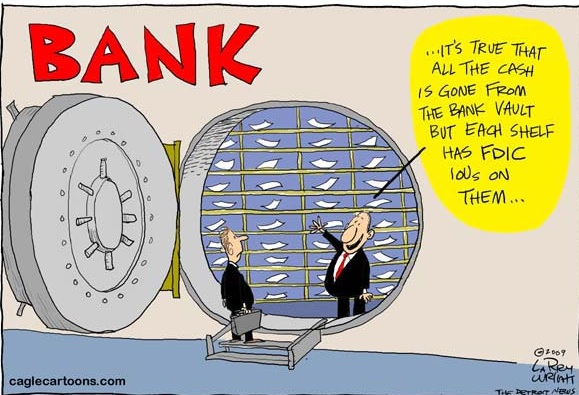

In a system without deposit insurance depositors have a big incentive to monitor their banks behaviour, to ensure they do not act in a manner which may endanger their solvency. (If the government didn’t promise to repay your money in the case that your bank fails, would you not be a little more concerned about how the bank uses your money?). In a system with deposit insurance this incentive is removed. Economists call this moral hazard. Moral hazard is when the provision of insurance changes the behaviour of those who receive the insurance in a undesirable way. For example, if you have contents insurance on your house you may be less careful about securing it against burglary than you otherwise might be.

Deposit insurance removes depositors incentive to monitor bank lending decisions because they are guaranteed to receive their money back. Instead, depositors are incentivised by the interest rate offered. Of course, those banks offering the highest interest rate will be those taking the greatest risks, and so banks are incentivised to finance the highest risk, highest return projects.

While higher interest rates may seem to benefit depositors due to higher returns (but not taxpayers – due to greater risks leading to more financial crisis and bailouts) it reality they do not. Instead of offering a higher rate of interest the private bank can offer a lower rate, because the deposit is risk free. This results in a subsidy to the banking sector – the value of which reached over £100bn in 2008.

So despite the fact that deposit insurance is intended to increase the stability of the banking system by preventing bank runs it may in fact make it more dangerous by encouraging risky behaviour from banks:

The U.S. Savings & Loan crisis of the 1980s has been widely attributed to the moral hazard created by a combination of generous deposit insurance, financial liberalization, and regulatory failure… Thus, according to economic theory, while deposit insurance may increase bank stability by reducing self-fulfilling or information-driven depositor runs, it may decrease bank stability by encouraging risk-taking on the part of banks. Banks are Different from Other Businesses

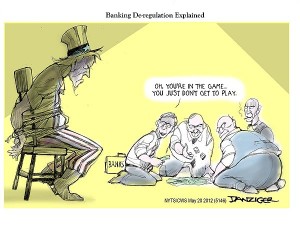

Jean Claude Trichet writes: Banks and banking rely on trust. But while trust takes years to establish, it can be squandered abruptly if a particular bank’s ethics are weak, its values poor, and its behavior simply wrong.

The events that triggered the 2008 global financial crisis, together with the subsequent scandals that have emerged – from the rigging of the London Interbank Offered Rate (Libor) to sanctions-busting and money-laundering – amount to a catalog of cultural failures within our financial institutions. Yes, extensive measures have been taken since the crisis to strengthen the financial system. But a profound weakness remains: To be blunt, it concerns the risk-taking culture that still prevails within some departments of global banks and in the financial system itself.

We fail to start our examination of banks with definition of what a bank is. A bank takes in other peoples’ money, which is why banks have to be regulated. They hold and invest that money. Earning 10-12 percent if considered reasonable. Banks now try to earn %25 percent. They simply can’t do that legally.

Too often, bank bosses’ promises to change the “corporate culture” and ensure their employees’ good conduct have not been matched by fully effective implementation. In too many cases, banks are still failing to fulfill their obligations in serving their communities and the public at large.

More regulation is not necessarily the best path forward: The rules and norms that define a “right” and “wrong” culture are beyond the wit of regulators and supervisory bodies It is not enough to strengthen legal compliance. Real change must go to the core of an institution’s day-to-day operations. Banks must change compensation practices that reward excessive risk; protect whistleblowers; recruit and train staff to reflect proper ethics; and ensure that their boards of directors play a more active oversight role.

Employees must understand instinctively what may be done and what should never be done. They must internalize a culture that values strict adherence to high ethical standards of conduct.

Banking regulators and supervisors also have a decisive role to play. They need to work with boards and senior management to ensure that major reforms are implemented and then consistently applied. Regular exchanges of views between oversight officials and the banks should be regarded as a crucial component of this process.

Carmen Reinhart writes: For the 189 countries for which data are available, median inflation for 2015 is running just below 2%, slightly lower than in 2014 and, in most cases, below the International Monetary Fund’s projections.

Most of the other half are not doing badly, either. In the period following the oil shocks of the 1970s until the early 1980s, almost two-thirds of the countries recorded inflation rates above 10%. According to the latest data, which runs through July or August for most countries, there are “only” 14 cases of high inflation (the red line in the figure). Venezuela (which has not published official inflation statistics this year) and Argentina (which has not released reliable inflation data for several years) figure prominently in this group. Iran, Russia, Syria, Ukraine, and a handful of African countries comprise the rest.

The risk for the world economy is actually tilted toward deflation for the 23 advanced economies in the sample, even eight years after the onset of the global financial crisis. For this group, the median inflation rate is 0.2% – the lowest since 1933.

While we do not know what might have happened were policies different, one can easily imagine that, absent quantitative easing in the United States, Europe, and Japan, those economies would have been mired in a deflationary post-crisis landscape akin to that of the 1930s.

Falling prices mean a rise in the real value of existing debts and an increase in the debt-service burden, owing to higher real interest rates. As a result, defaults, bankruptcies, and economic decline become more likely, putting further downward pressures on prices.

The 2.2% price decline in Greece for the 12 months ending in July – the most severe example of ongoing deflation in the advanced countries and counterproductive to an orderly solution to the country’s problems.

Median inflation rates for emerging-market and developing economies, which were in double digits through the mid-1990s, are now around 2.5% and falling. The sharp declines in oil and commodity prices during the latest supercycle have helped mitigate inflationary pressures, while the generalized slowdown in economic activity in the emerging world may have contributed as well.

But it is too early to conclude that inflation is a problem of the past, because other external factors are working in the opposite direction.

Given that most emerging-market countries’ trade is conducted in dollars, currency depreciation should push up import prices almost one for one.

At the end of the day, the US Federal Reserve will base its interest-rate decisions primarily on domestic considerations. While there is more than the usual degree of uncertainty regarding the magnitude of America’s output gap since the financial crisis, there is comparatively less ambiguity now that domestic inflation is subdued. The rest of the world shares that benign inflation environment.