San Francisco Fed President says it will take the US Fed six years to reduce its bloated balance sheet.

It will take the U.S. central bank at least six years to reduce its bloated balance sheet back to more a normal size, San Francisco Federal Reserve Bank President John Williams said.

“Our plan is to shrink the balance sheet ‘organically,’ if you will, through the maturation of the assets,” Williams said in the text of remarks Friday in Santa Barbara, California. “It’s likely going to take at least six years to get the balance sheet back to normal, which is in keeping with the overall approach to removing accommodation gradually.”

The Federal Reserve is slowly weaning the economy off of ultra-easy monetary policy that saw it hold interest rates near zero for seven years and balloon the balance sheet to around $4.5 trillion through three rounds of buying mainly Treasuries and mortgage-backed securities. Officials took a major step in December, raising interest rates for the first time since 2006, and said they’ll wait until the process of policy normalization is well under way before beginning to allow excess balance-sheet holdings to roll off.

He said the economy “still has a good head of steam,” that he expected would help keep the unemployment rate on track to decline to around 4.5 percent by mid-year.

“Looking forward, I see a labor market that’s growing ever stronger and will reach maximum employment on a broad set of measures very soon,” he said.

Even so, Williams argued that the economy still needed support from Fed policy to help it overcome headwinds from slower growth abroad and the fallout from a stronger dollar, which was why officials expect a gradual pace of rate hikes.

Even at their peak, rates are likely to be low by historical standards — perhaps just 3 percent or 3.5 percent, compared to the 4 percent to 4.5 percent that was historically normal, Williams said.

Participation Rate

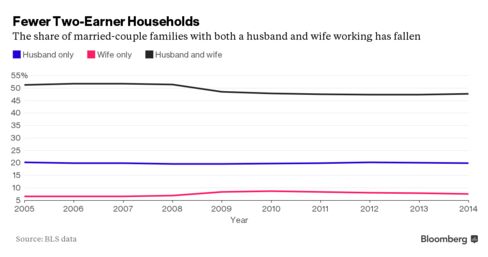

The labor force participation rate, which has plummeted and is near its lowest level since the 1970’s, is also unlikely to rebound to a more normal level, Williams said. He attributed the change to the aging of the U.S. population, the fact that younger people aren’t working as much as they used to, and the fact that people are increasingly deciding to have single-income families.

“Overall, the evidence suggests that, even with a quite strong economy, we aren’t likely to see a significant number of people come back into the fold,” Williams said today.

Despite such changes, he said the economy has made significant progress, noting that the U.S. has added more than 13 million jobs since 2009, “virtually all of them full-time.”

Even as full employment draws near, inflation remains far below the Fed’s 2 percent target, rising just 0.4 percent in November from a year earlier. Still, Williams says he expects that inflation will be at or near target by the end of next year.

“There are reasons for the low level of inflation, in particular the rise in the dollar and the fall in oil prices,” Williams said. “Those effects should peter out, but they’ve had a downward influence on inflation at a time we’ve needed it to rise.”