Kenneth Rogoff writes: Why do the comments of major economies’ central bankers command outsize attention nowadays? It is not as if they change interest rates all of the time. Nor have they developed new, more robust models for analyzing the economy. On the contrary, major central banks’ growth and inflation forecasts in the years since the financial crisis have consistently overestimated both growth and inflation – and by wide margins.

There are many good reasons for the attention lavished on monetary policymakers, including the rise of central-bank independence, public acceptance of the need to appoint highly competent technocrats to oversee the money supply, and the deepening of financial markets. And many central bankers have been rightly lauded for their role in preventing a global meltdown during the financial crisis.

Even so, given the numerous uncertainties surrounding macroeconomic forecasts and the effects of policy instruments (not least quantitative easing), many academics find it puzzling that central bankers’ speeches and statements generate so much fanfare. Moreover, central bankers bear a share of the blame for the crisis in the first place, mainly owing to lax regulatory policy.

Many central bankers portray former US Federal Reserve Chairman Alan Greenspan (who served from August 1987 until January 2006) as the culprit, saying that he projected an image of central-bank omnipotence that is not warranted in theory or practice. But this critique is overblown: Greenspan is long gone, but the focus on central-bank pronouncements is greater than ever.

What, then, is going on? I would argue that, in addition to all of the factors listed above, three further considerations should be noted. For starters, the public perception that central bankers are omniscient makes them an attractive whipping boy for politicians. Moreover, the digital revolution in media has elevated the role of business news, one of the few profit centers for print and broadcast journalism in many countries. Central bankers’ pronouncements are of interest to businesspeople – especially in the financial sector – and businesspeople are of interest to advertisers.

Finally, and perhaps least appreciated, is the fact that central-bank policy pronouncements are almost unique in having clear and predictable effects on financial markets, at least in the very short run.

Some economic indicators, such as unemployment or inflation data, are indeed immediately important for central banks, because they may directly concern their mandates, and therefore have rather predictable effects. But much information is simply noise. This makes policy opinions that come straight from the horse’s mouth almost uniquely valuable.

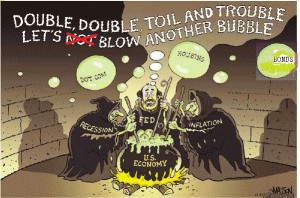

In short, there are many good reasons why central bankers receive so much media focus, including their relative independence and generally solid performance. But there are also other reasons having to do with politicians’ need for scapegoats, the media’s struggle to reinvent itself in the Internet age, and central-bank pronouncements’ predictable short-term effects on financial markets. These other factors have combined to create a bubble around central-bank pronouncements and decisions that grossly exaggerates their economic significance.

Is this a bubble that central bankers should worry about? The answer is clearly yes. The news bubble is of particular concern, because it reinforces the idea that central bankers somehow care disproportionately about financial markets, which is generally not the case.

Most central bankers really are targeting growth, inflation, and financial stability, if not necessarily in that order. The political bubble is an inevitable product of central-bank independence, and preventing monetary policy from becoming a target for elected officials requires constant effort. The predictability bubble is perhaps the trickiest to navigate, though my instinct is that less would be more. Exaggerated importance is one kind of bubble that central bankers should always be eager to burst.