DIgital Gold by Nathaniel Popper. The New York Public Library had a very interesting discussion of the book with the author, a Bitcoin technology expert and an investor. It is available as a livestream.

Even the experts have a difficult time describing the blockchain technology, which is a record of all the transactions that take place. It is this technology that will probably survice even if the currency does not. It provides the cheapest and safest way for credit card and similar transactions to be recorded and paid.

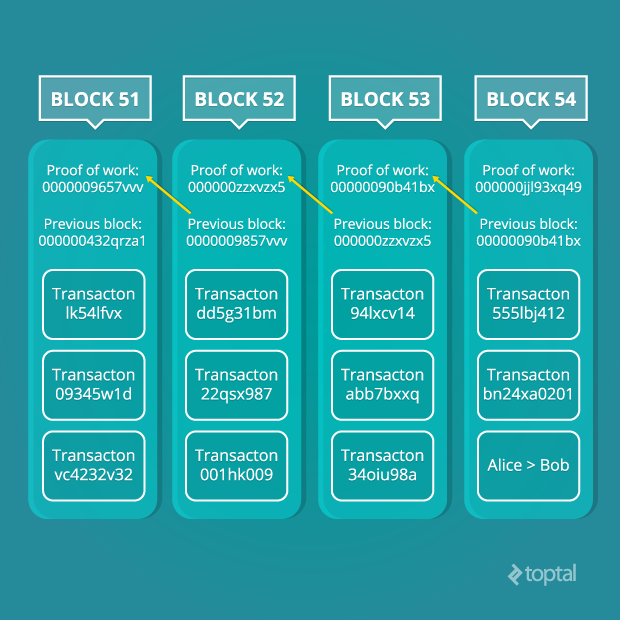

The blockchain is seen as the main technological innovation of Bitcoin, since it stands as proof of all the transactions on the network. A block is the ‘current’ part of a blockchain which records some or all of the recent transactions, and once completed goes into the blockchain as permanent database. Each time a block gets completed, a new block is generated. There is a countless number of such blocks in the blockchain. So are the blocks randomly placed in a blockchain? No, they are linked to each other (like a chain) in proper linear, chronological order with every block containing a hash of the previous block.

To use conventional banking as an analogy, the blockchain is like a full history of banking transactions. Bitcoin transactions are entered chronologically in a blockchain just the way bank transactions are. Blocks, meanwhile, are like individual bank statements.

Bitcoin blockchain is the technology backbone of the network and provides a tamper-proof data structure, providing a shared public ledger open to all. The mathematics involved are impressive, and the use of specialized hardware to construct this vast chain of cryptographic data renders it practically impossible to replicate.

All confirmed transactions are embedded in the bitcoin blockchain. Use of SHA-256 cryptography ensures the integrity of the blockchain applications – all transactions must be signed using a private key or seed, which prevents third parties from tampering with it. Transactions are confirmed by the network within 10 minutes or so and this process is handled by bitcoin miners. Mining is used to confirm transactions through a shared consensus system, and usually requires several independent confirmations for the transaction to go through. This process guarantees random distribution and makes tampering very difficult.n.

The potential is more or less obvious. Decentralizing trust is a big thing, allowing the creation of vast, secure networks without a single point of failure. You can think of them as an additional layer of the internet, a layer that can be used for authentication, signage, secure communications and content distribution, financial transactions and much more.

Blockchain technology could allow developers a simple way of outsourcing security. For example, instead of creating secure IoT devices and networks, much of the heavy lifting could be effectively offloaded to the blockchain, freeing up resources on the client’s side and speeding up development.

The elusive goal for all blockchain developers is to make the technology just as seamless and unobtrusive as internet protocols. For example, how many people realize they are using TCP/IP every time they start browsing the net? This is the ultimate goal – to make the use of blockchain technology invisible to the end user. Blockchain technology can become yet another layer added to various products and services in order to provide more functionality and security, while saving resources and developer man-hours.

Bitcoin and blockchain technology are certainly “out there,” and some developers view them as the next frontier. Developing a use case for bitcoin and blockchain technology applications could prove profitable in the long run, and many are eager to enter the space.

It’s simple – they are both getting a head start! Bosch and IBM, are looking into ways of harnessing blockchain technology as part of their Internet-of-Things (IoT) development programs. Microsoft has also interested in the technology behind bitcoin for distributed, connected devices (or IoT devices). Samsung is on board as well, and the Korean consumer electronics giant showed off blockchain tech at CES 2015, alongside IBM.